The post A Beginner’s Guide: Understand What is Blockchain Technology in 3 Minutes! appeared first on Coinpedia Fintech News

The beauty of technology is that it is committed to producing tools and processing activities, and it just becomes better over time. Once in your lifetime, you might have heard or come across the term “Blockchain”.

“Blockchain”, isn’t it, sounds like a hardcore buzzword. OR too techie!!!

But do you know, What is it? & Why it’s introduced? Why it is becoming vital in the digital world.

Well, let me help you understand that in a simple and easier manner.

In 1991, blockchain was introduced to overcome the flaws of a centralized network, which possesses a single point of failure, if the primary server crashes, the whole network will probably close down. Then the client nodes will not be apt to send, receive, or function user operations on their own.

To strengthen the centralized security system & decreasing the use of that middleman transaction system, Stuart Haber & W Scott Stornetta cryptographically secured a chain of blocks, i.e. later recognized as Blockchain (Decentralized Network).

Table of contents

- What is Blockchain Technology?

- Why is Blockchain Popular?

- What are the Different Types of Blockchain Networks?

- How Does Blockchain Work?

- Why is Blockchain Important?

- Features of Blockchain Technology

- Numerous Use Cases of Blockchain Technology

- How Blockchain is Transforming the Data Center Architecture

- Benefits of opting for Blockchain Networks in Business

- FAQs

Let’s understand this with a real-life problem that is faced by many countries these days, i.e. tampering with voting.

Tampering of Votes

The transparency of the election is one of the main issues that many countries face. I’m sure there have been a few occasions when you heard about several instances of incorrect voting counts, hacks of voting machines, or forced voting.

To reduce such flaws, blockchain technology could be a game changer. But, How?

Let’s understand this by an example;

Consider an election held at your college for the post of College student president & the college committee decides to use a blockchain system for conducting elections to maintain the transparency & reliability of elections.

Because Blockchain-based voting systems have the potential to eliminate any of these ( hacks to voting machines or miscounts on voting, as well as forced voting) problems.

When voting occurs on the Blockchain network, it will be monitored in real-time & is unable to be changed. However, it will be easier to see the differences in results, so the winners of elections can easily be identified.

Through the use of a blockchain-based voting system, the college election conducting committee can ensure the anonymity of voters through a transparent crypto algorithm. So the issue with elections is, voter privacy will be maintained.

What is Blockchain Technology?

Beginning of Blockchain in the Real World

Well, Stuart Haber & W Scott Stornetta developed the idea of blockchain as a research program in the year 1991 and Satoshi Nakamoto later executed it for the first time in the year 2008.

He had the concept of developing a digital platform that could facilitate the transfer of money without having to involve any central authority. This blockchain technology was initially introduced in Bitcoin in 2009.

Concept of Blockchain = ( Block + Chain )

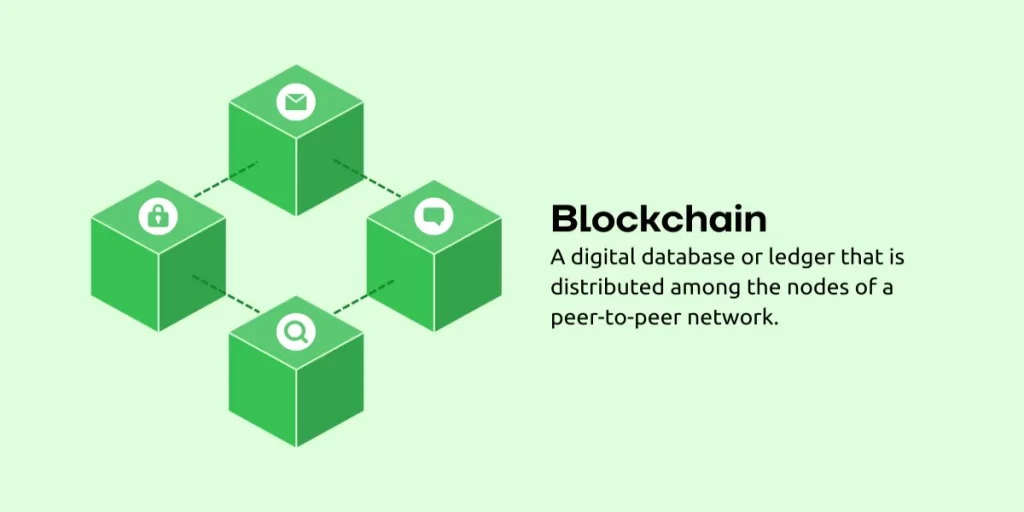

Blockchains are unchangeable digital ledgers that keep records or transactions across multiple locations within a network of computers. Every validated transaction is added to a place called a “block” and the linking of these blocks into a chain of data creates the blockchain.

Eventually, there are three main elements that make up the blockchain, i.e. a record, a block, and the chain.

- Record:- can refer to any type of information, such as the details of a deal or exchange between two individuals.

- Blocks:- are a collection of information that is put together. They usually share common characteristics.

- Chains:- are formed when all blocks are connected.

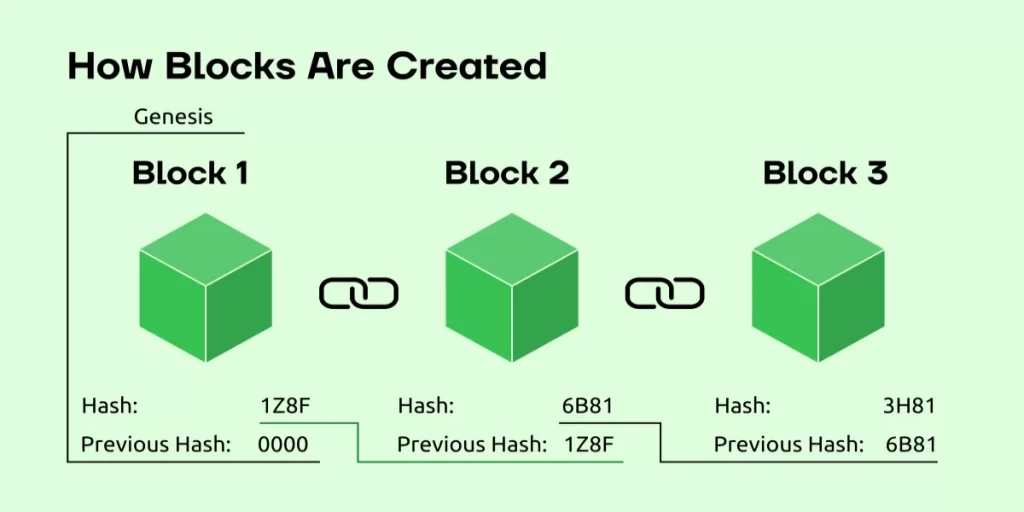

When a single block is made, it contains Data, Hash number & Previous block Hash code (Genesis Block).

- Data:- A data consists of transaction details of the sender, receivers & the amount to be paid.

- Hash Value:- However, it is said, that every new record is a “block” that has a unique hash(#). Such hash value is generated by a mathematical procedure that takes in digital information and creates a string of numbers and letters.

- Genesis block:- First block which is referred to by the name of the “genesis block”, because it does not contain any previous block hash value.

One of its main benefits is that the data cannot be changed without the consent of all the parties that are involved. Users are only permitted to alter areas of the blockchain they “own” through the ownership of private keys needed for altering block data.

To understand more in-depth about blockchain & how blockchain work, it is more important to know the different types of blockchain & their use-case.

Why is Blockchain Popular?

Suppose, you wish to transfer funds to your family members or friends using the bank account. You’ll sign in to online banking, and make the transfer of funds to another person by using the account number. Once the transaction has been completed your bank will update the transaction’s records.

It’s not difficult, isn’t it?

But there is a problem that is often overlooked by the majority of us.

These kinds of transactions could be manipulated quickly. People who are aware of this reality are generally aware of these kinds of transactions. However, this is the primary reason why Satoshi Nakamoto invented Blockchain technology,

Technology-wise, Blockchain is an electronic ledger that has been receiving a lot of attention and popularity in recent years.

But, Why is it becoming so well-known? & What’s thee blockchain strategy?

Let’s explore it to understand the entire idea…

The recording of data and recording transactions is a crucial element of the business. Most of the time, these blockchain records are managed in-house or through an outside party such as bankers, brokers, or lawyers. This can result in a significant increase in the time, expense, or both of the company.

It is good news that Blockchain can cut out this lengthy procedure and allows for faster transfer of multiple transactions which saves both cash and time. A majority of people think that blockchain and Bitcoin are able to be used interchangeably, however, it’s not the situation.

Blockchain is the tech that is capable of supporting different applications in diverse industries such as supply chain, finance, manufacturing, etc. But Bitcoin is a form of currency that is dependent upon Blockchain technology to protect itself.

Benefits Of Blockchain Technology

- Highly Secure

It employs an electronic signature feature that allows for secure transactions, making it virtually impossible to corrupt or alter the information of an individual through other users who do not have a digital signature.

- Decentralized System

Conventionally, you must have permission from regulatory bodies such as the bank or government to conduct transactions. However, when you use Blockchain transactions, transactions are made by the agreement of the users, resulting in safer, smoother, and more efficient transactions.

- Automation Capability

It is programmable and will create a sequence of events, actions, and automatic payments when the requirements of the trigger are met.

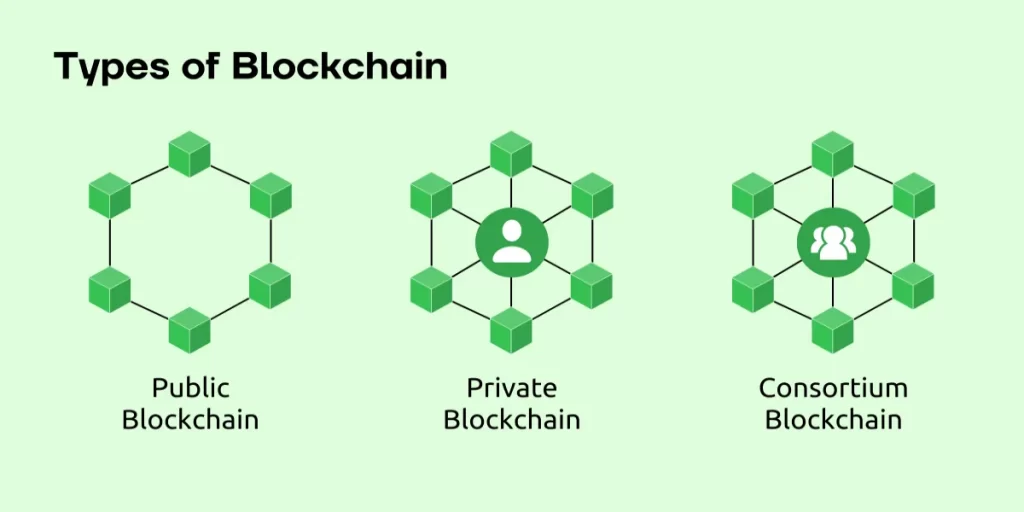

What are the Different Types of Blockchain Networks?

There are three fundamental types of blockchain networks that in functioning, i.e. Public blockchain network, private blockchain network & consortium blockchain technology.

Public Blockchain Networks

A permission-free or public blockchain is one in which anyone can be a part of the network without limitations. The majority of cryptocurrency types operate on a public blockchain network which is controlled by consensus algorithms or rules.

Ex:- When voting is done on a Blockchain, the government & public can monitor each & every vote in real-time & is unable to be changed. However, these will ensure transparency and trust in the minds of the public.

And this technology will eliminate the possibility of altering any election. So, the winners of elections are easily identified.

Benefits of Public blockchain networks

- Voting:- Governments can use the blockchain of the public to vote to ensure transparency and trust.

- Fundraising:- Initiatives or businesses can make use of the blockchain, which is a public Blockchain to enhance the transparency and confidence of their customers

Permission or Private Blockchain Networks

A permissioned private or blockchain network allows organizations to form limitations on who has access to the blockchain’s information. Only users with permissions can access certain sets of information. Oracle Blockchain Platform is a secured blockchain.

Not everything that is on the blockchain is accessible to everyone & that’s where a private blockchain or a permissioned or private blockchain network comes into play.

Ex:- Consider, you have a bank account in a federal bank & the bank is using blockchain technology to make the banking system more reliable, secure, faster & trustworthy for users.

You expect that your bank details (account balance, private transactions history, etc.) be kept private, which has been only accessible to you & your bank. In such a privacy-maintaining place a private blockchain or a permissioned blockchain comes in use.

Benefits of private Blockchain networks

- Supply Chain Management:- A private blockchain could be utilized to manage a business’s supply chain.

- Asset Ownership:- Blockchains that are private are a way to monitor and confirm assets.

- Internal Voting:- Internal Voting is possible using an encrypted blockchain.

Consortium or Federated Blockchain Networks

A blockchain network in which there is a consensus procedure (mining procedure) is tightly controlled by a set of pre-selected nodes(miners) or by a selected number of stakeholders.

Ex:- Consider you want to make any changes in your Date of Birth (DoB), & the previous DoB copy is uploaded on the blockchain. However, to make a new change to an existing DoB, you need to provide proof of work, which defines your change.

If all the nodes(miners) found it to be a reliable change & voted for your change majoritively, then the alternation will be accepted or if they found that you are tampering with the data, then it will be rejected.

Benefits Consortium of Federated Blockchain Networks

- Banking and Payments:- A group could be created by banks that work together. They control the nodes that will verify transactions.

- Research:- A blockchain consortium can be used to exchange research results and data.

- Food Tracking:- It’s suitable for tracking food.

Every Blockchain comes with distinct advantages which is why there isn’t a simple solution to the issue regarding which Blockchain to select. Be sure to consider your requirements to make the right decision.

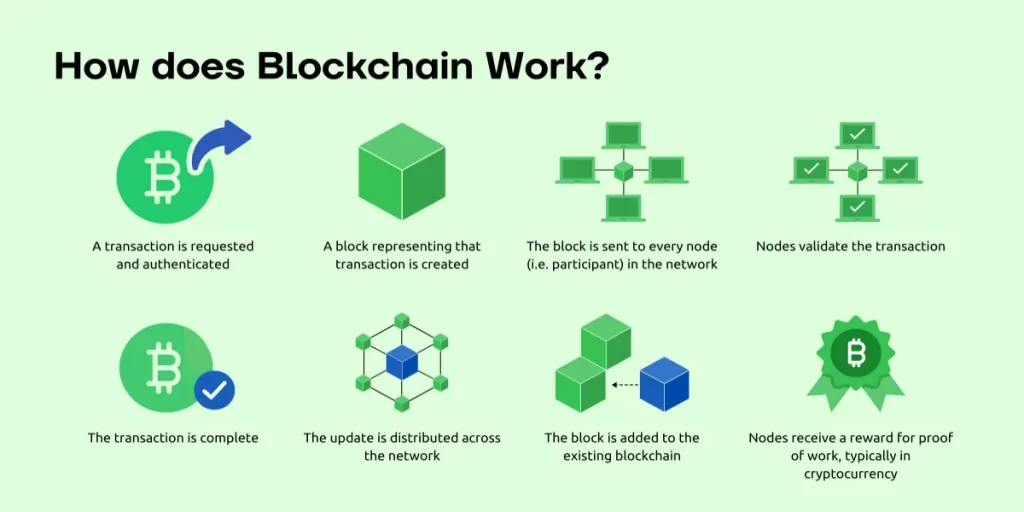

How Does Blockchain Work?

A few people have described blockchain as “the internet thing” which I believe is a great metaphor.

Blockchains allow a community of people to share potentially crucial information with tamper-proof security. You must however have an encrypted, private key to only edit the blocks that you “own.”

For instance, a cryptocurrency-based blockchain records data about crypto transactions, which contains the transactions of the recipient, trader, and amount of capital being swapped.

Working Process of the Blockchain Networks

- Firstly the transaction is requested & validated via the Blockchain network.

- Then the new block is formed to represent the record transactions.

- The newly formed block is then transmitted to every Node (miner) on the blockchain network.

- These Nodes verify the newly formed block & the financial transactions.

- (In most cases) nodes receive a bounty due to the proof-of-work system.

- These new verified blocks will be then chained to the blockchain.

- The alterations to the blockchain are publicized throughout the network.

- Then successfully the validated transactions are completed.

To understand the working of blockchains, let’s take the example of bitcoin blockchain transactions.

Roy is looking to transfer 5 Bitcoins to John through a blockchain based-network.

- The input: – Roy’s private address for his coin that he at the time holding coins he would like to spend.

- The output: – John’s public key, or coin address.

- The amount: – the number of coins Roy would like to spend.

Okay – but what is the process?

Step 1:- Roy will transfer five Bitcoin to John via a blockchain-based networking system.

Step 2:- He will send a message containing the details of the transaction by using his private key. Thus, the message will contain all details of the transaction’s input, and output as well as the amount to be sent.

Step 3:- The transaction records are then broadcast to all P2P (Peer to Peer network) participating computers on the particular blockchain network telling them that the number of Bitcoins in the account of Roy should decrease by 5 and the total amount in John’s account should rise by 5.

Step 4:-. Each computer within the network will be notified and then apply the transaction record to their ledger copy and update the balances of the account.

Step 5:- Hence with these successful transaction data, a new block is then added to an existing chain and is not able to be altered in any way.

Why is Blockchain Important?

We’re all comfortable sharing data via a decentralized online platform, i.e. the internet. However, when it comes to the transfer of value, e.g. Capital, proprietorship rights, intellectual property, etc. We’re usually required to rely upon traditional methods, i.e. our centralized institutions, such as governments or banks.

“PayPal” is the most obvious example, as it needed the integration of the bank account or credit card to serve as a viable option.

You know the worst part…

Centralized networks can’t scale past a specific point, since the only path to do so is to expand additional storage, bandwidth, or processing power to the main server & which will indirectly raise the expense of operation.

Then what’s the blockchain solution? How will blockchain help? Blockchain systems presents a fascinating substitute for decreasing the use of that “middleman” transaction.

- It accomplishes this by fulfilling three crucial roles, i.e. keeping track of online transactions and creating identities, and creating smart contracts, which are normally performed by the financial sector.

- It has huge importance in the world because the financial transactions services industry is the largest segment of the economy based on market capitalization.

- If we could replace even a small portion of this with a blockchain network would cause a massive change in the financial services industry as well as a huge improvement in efficiency.

- While opting for blockchain technology, it’s not that easy for hackers to gain access to the data and, even if hackers gain access, the data is easily obtained.

Blockchain’s benefits for supply chain management have impressed us over the last few years. The revolutionary technology provides better and more transparent ways to manage inventory as well as keep track of all transaction that occurs.

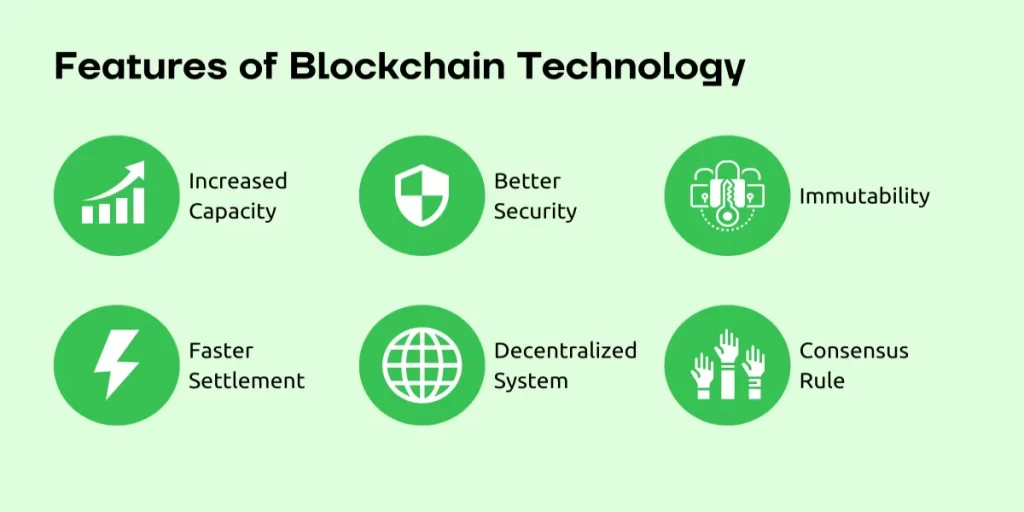

Features of Blockchain Technology

1. Increased Capacity

The most striking thing about Blockchain systems is the fact that it enhances the capabilities of the entire blockchain network. This is due to the fact that there are many computers operating together, it gives greater performance, compared to the devices being centralized.

2. Better Security

Blockchain technology is believed to be more secure than the alternatives due to the absence of one only one point of fault. Blockchain is a distributed network of nodes. Therefore, information is distributed through not just only one, but many nodes this ensures that even in the event that one node is compromised or damaged in any way, the integrity of the data isn’t affected.

Blockchains such as Bitcoin maintain their records in a perpetual state of forward momentum.

3. Decentralized System

Decentralized technology offers you the ability to store your assets on an online network, without the supervision and control of one individual or organization. Blockchain technology is an extremely effective tool for centralizing the internet, which can create a completely revolutionizing world of the internet.

4. Consensus Rule

The consensus algorithm is the one that makes blockchain technologies extremely efficient. It is a fundamental element of all blockchains and is in fact a key feature. In simple terms, it is an important decision-making process that affects the nodes that are active within the system. The nodes involved can reach an agreement swiftly and generally faster.

5. Distributed Ledger technology (DLT )

Distributed public ledgers contain information about transactions, and also include the participants in the public. The distributed ledger technology permits anyone with access to see the ledger. This makes the process reliable and transparent.

Numerous Use Cases of Blockchain Technology

Here are the most common Blockchain technology use cases classified under distinct industries/applications:-

Banking

Payment processing and money transfer are among the best Blockchain technology applications. Blockchain network allows instantaneous transactions in real-time.

It can provide an opportunity for non-trusted parties to reach an agreement about the state of a database without the need for intermediaries, like banks or financial institutions. Blockchain technology allows instantaneous transactions in real-time.

With a ledger that does not have a single person managing its blockchain technology can provide specific financial services such as securitization, payments, or even payments without the need for banks

Logistic

Today, most logistics companies offer only the details about their major locations, such as collection centers, city hubs, as well as sorting services. The precise location details are not known and in the event of a system failure, all data is lost.

With blockchain technology, you can develop a system to collect information about the location from a variety of interconnected systems, and then provide exact information about the location to clients. The applications of this project could be extended to other areas, such as airlines to track lost luggage, car rental to track rented cars, etc.

Real Estate

The real estate market is facing numerous issues, including the need to connect both buyers and sellers. Presently, buyers have to meet with the broker or seller to conclude the deal. The time frame can vary between a few months and one year.

It requires an enormous amount of time for the completion of the documents which could be affected by inaccurate information entered. There are difficulties when it comes to verifying the ownership of the property. Additionally, fraud can occur in a variety of ways and cost the buyer money.

To tackle these problems to overcome these challenges, a decentralized blockchain ledger can be beneficial, as it has an excellent use-case for blockchain.

Transparent and Genuine Charity / Crowdfunding

A lot of fake charities pose as genuine and steal cash from innocent people under the guise of charity. People are generally eager to give money to a worthy cause but aren’t certain of whether the money will be used for the benefit of the poor.

Blockchain technology can provide transparency to trusts for charitable donations. The donors can follow the route of the money in real-time and verify if the money is reaching the hands of those who need it or not.

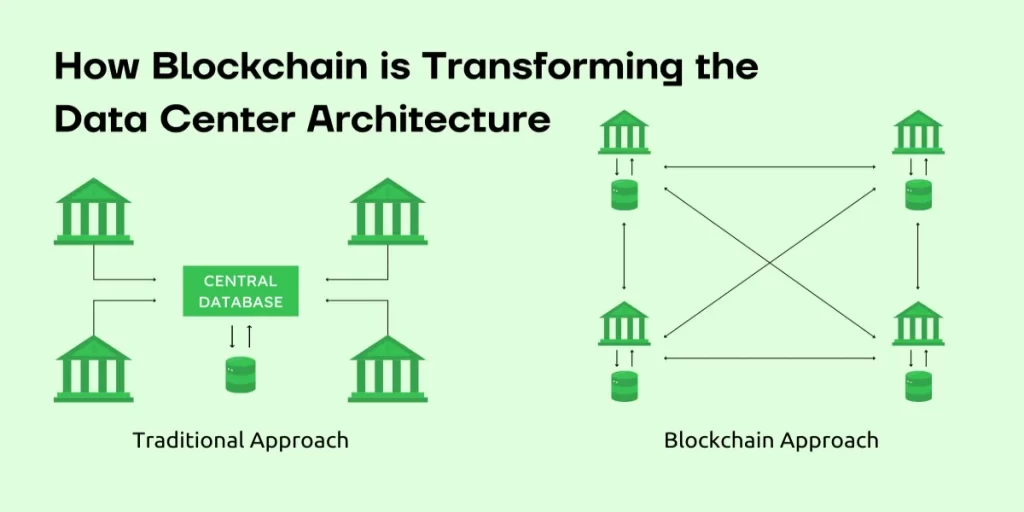

How Blockchain is Transforming the Data Center Architecture

With regards to the data center structure, the blockchain has a unique method of storage of data. However, as we know that blockchain technology utilizes decentralization to store and manage information.

We even know that a blockchain network could consist of hundreds or even thousands of computers spread all over the globe in different places.

Consider, if a hacker decides to attack a blockchain network successfully, he/she must shut down several computers on the network, and even then, all blockchain-related data is secure, as it is encrypted, which reduces security risks.

These benefits directly challenge traditional storage in data centers. As the data center stores a massive quantity of data in one place. This makes them more in danger of natural disasters and interruptions in local power.

To increase safety and prevent loss of data, organizations may duplicate data and store it elsewhere; however, this procedure is time-consuming and expensive and creates an overflow of data that needs to be secured.

Blockchain data storage can provide greater levels of redundancy, safety, dependability, and transparency. The distributed nature of blockchain storage allows users to have greater levels of control over the location they store their data. However, for now, it is a lot more secure security for data than in-house or cloud storage.

Benefits of opting for Blockchain Networks in Business

Here’s a list of the top advantages you can realize when implementing Blockchain technology in your business:

- This is an unalterable digital public ledger. This means that once the transaction is recorded it is not able to be altered

- Due to the feature of encryption, Blockchain is always secure

- The transactions are executed immediately and without delay, since the ledger updates automatically.

- Because the system is decentralized there is no need for an intermediary fee.

- The authenticity of transactions is confirmed and verified by the participants

Conclusion

Businesses are increasingly focused on the best ways to utilize Blockchains to generate fresh revenue streams. As blockchain adoption is becoming a household name and has a variety of practical applications being developed & studied. The demand for Blockchain technology is increasing, and the entire community’s eager to embrace it.

However, now is the ideal time to let companies ride on the wave of change. Businesses should be investigating this technology and consider ways to use it to enhance their business. This will help ensure that they do not lose their place in the market, and also allow them to expand their businesses quickly.

FAQs

Blockchain technology could change our interactions with the online world. Blockchain technology can change the way we share and store data which makes it an essential element of the digital future.

Blockchain is a distributed, decentralized, and public digital ledger which records transactions across multiple computers so that the information cannot be modified in retrospect without altering the subsequent blocks or the consensus for the entire network.”

Blockchain allows users to trade directly with one another through a database of transactions that are kept in a ledger shared by all. This removes the need for middlemen such as banks and stock exchanges.

Blockchain technology refers to an electronic ledger that uses data structure, which can simplify our transactions. It permits users to alter the ledgers in a safe manner without the assistance of a third party. It lets you use cryptocurrency for free through a decentralized ecosystem.

There are at present more than 10,000 cryptocurrency systems operating on the blockchain. It has been demonstrated that blockchain can also be an effective method for keeping track of other kinds of transactions.